Orwell slagging off Gaudí’s Sagrada Família

This made me giggle:

This made me giggle:

Earlier today, I was combing through a working paper, using Claude Code to clean up the formatting and check grammar and writing (LLMs are wonderful for non-...

They were careless people, Tom and Daisy — they smashed up things and creatures and then retreated back into their money or their vast carelessness, and l...

The Lincoln Institute of Land Policy’s Land Lines magazine published an interview with me this month. Jon Gorey asked me about some of the more counterintuit...

One of the highlights of my year — for the tenth year running — is the Real Estate Finance and Investment Symposium that the Cambridge Real Estate Research C...

One pitfall of using Claude Code and other AI tools is that they make me lazy. The output is slick, useful, and smoothly integrated. The machines tries to gi...

Over the last few months, I have been working intensively with Claude Code, ChatGPT, and other AI tools. It has been a wild learning experience, and at times...

I have been looking at the ProudlyHuman de minimis standard and was somewhat surprised that the otherwise purist pro-human stance allows for using AI “to sea...

Under active development — findings and figures may change.

AI is changing how research gets done. But like weight loss drugs, it’s hard to tell from the outside whether the results come from the jab or the gym.

Spoiler alert. A Friday afternoon rant.

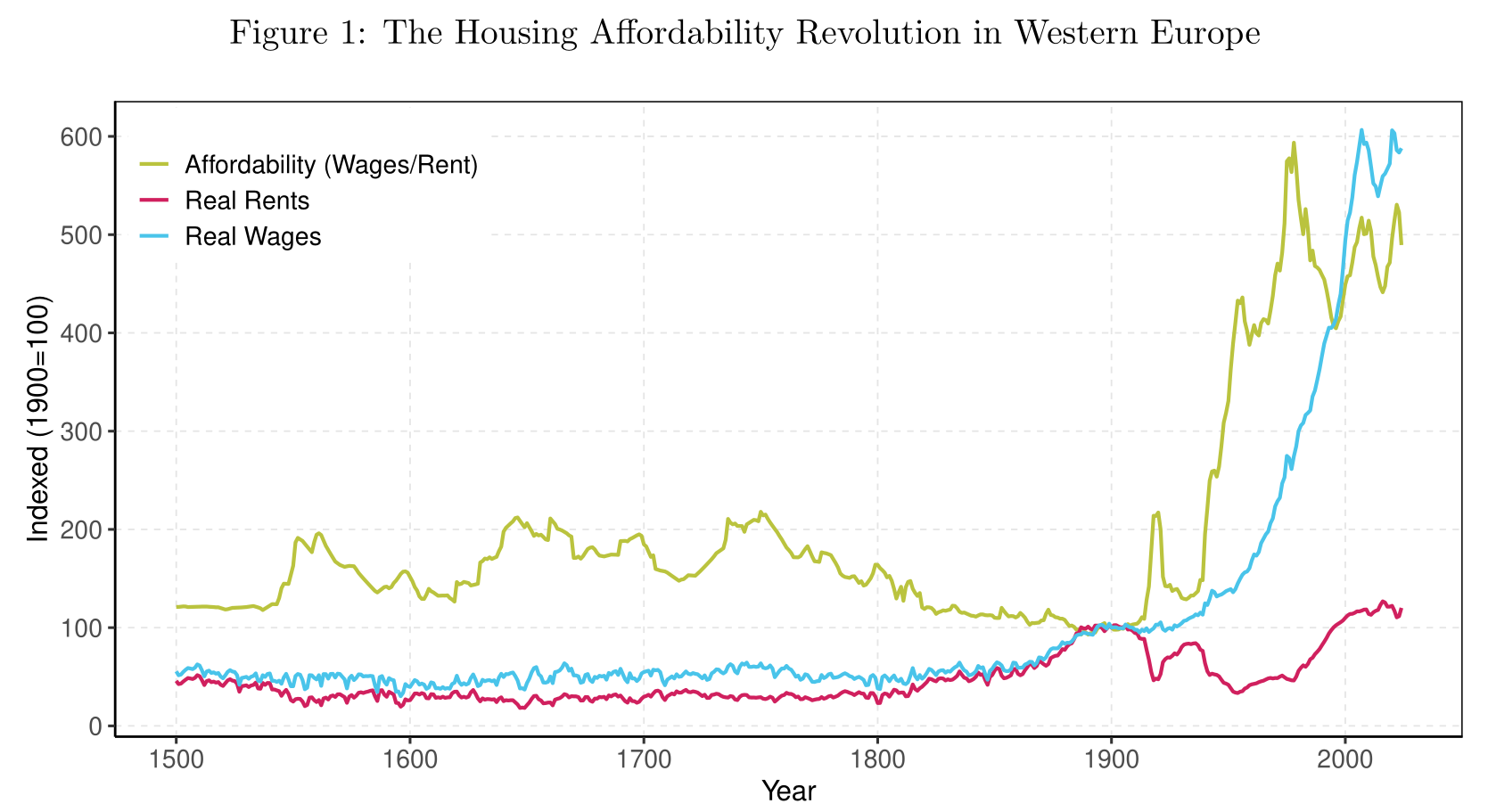

New version of Working paper out: 500 years of rents, wages and housing standards show how housing became cheaper yet less affordable for many. Overall, hous...

Today, we had a discussion about how teaching needs to evolve in these AI enabled time. As researchers and educators we are painfully aware of two AI-related...

The fourth Edition of the Geltner et al. CRE textbook is finally in production. And the ‘al.’ now includes (Lindenth)al…

Missing data are pervasive in commercial real estate research, yet common practice remains to discard incomplete observations or fill gaps with crude imputat...

I have learnt a lot from David Geltner over the last 20 years.

This made me smile.

Piet Eichholtz and I wrote this short piece on the impact of changing demographics on house prices many years back. Some people still ask me for a copy, so I...

It happens so often, stings every time, and should not slow you down…

Maybe, someone has used this term before. If not, I would like to suggest “ultra-processed data.”