Talk: AI in the research process

AI is changing how research gets done. But like weight loss drugs, it’s hard to tell from the outside whether the results come from the jab or the gym.

AI is changing how research gets done. But like weight loss drugs, it’s hard to tell from the outside whether the results come from the jab or the gym.

Spoiler alert. A Friday afternoon rant.

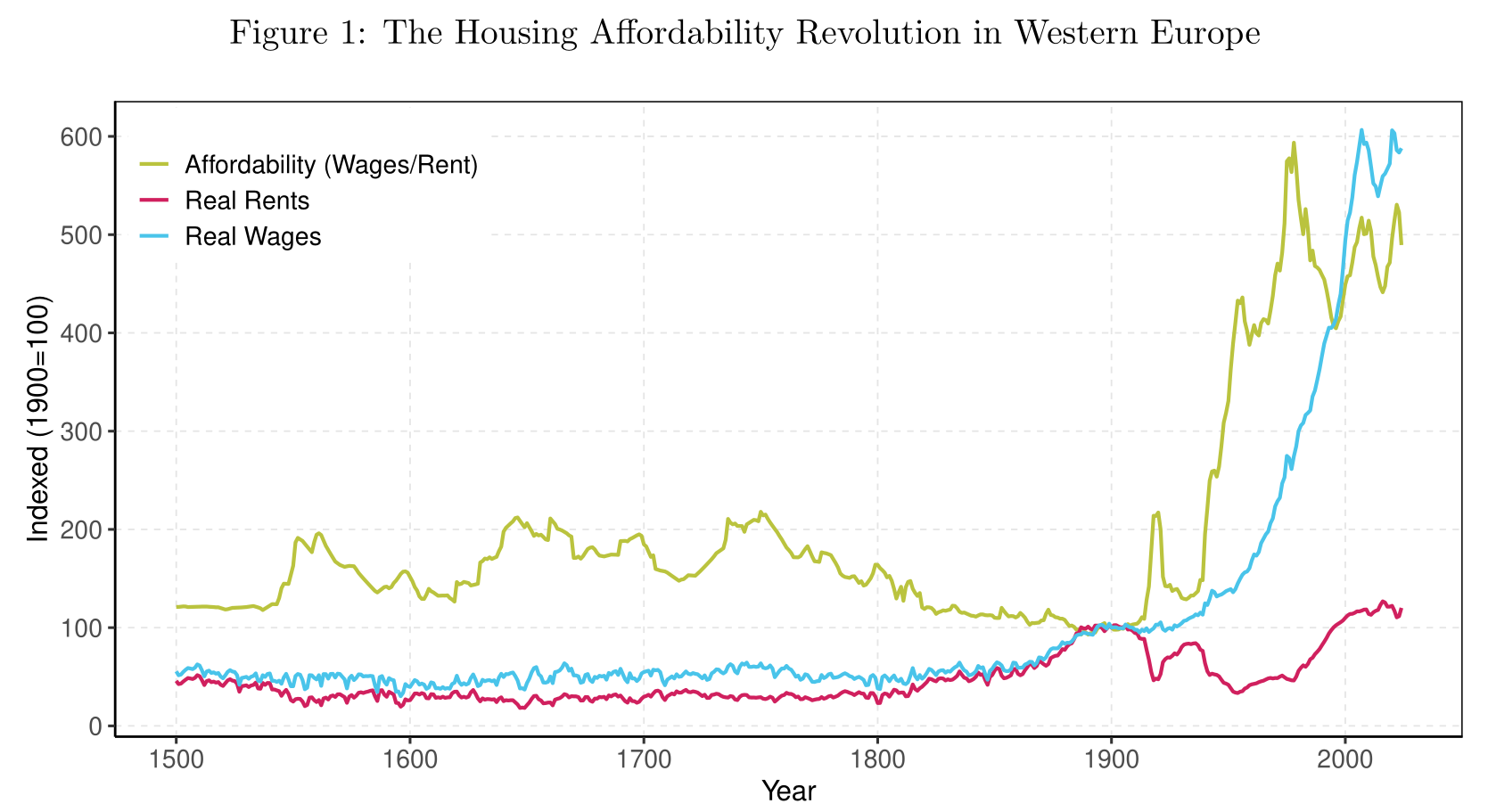

New version of Working paper out: 500 years of rents, wages and housing standards show how housing became cheaper yet less affordable for many. Overall, hous...

Today, we had a discussion about how teaching needs to evolve in these AI enabled time. As researchers and educators we are painfully aware of two AI-related...

The fourth Edition of the Geltner et al. CRE textbook is finally in production. And the ‘al.’ now includes (Lindenth)al…

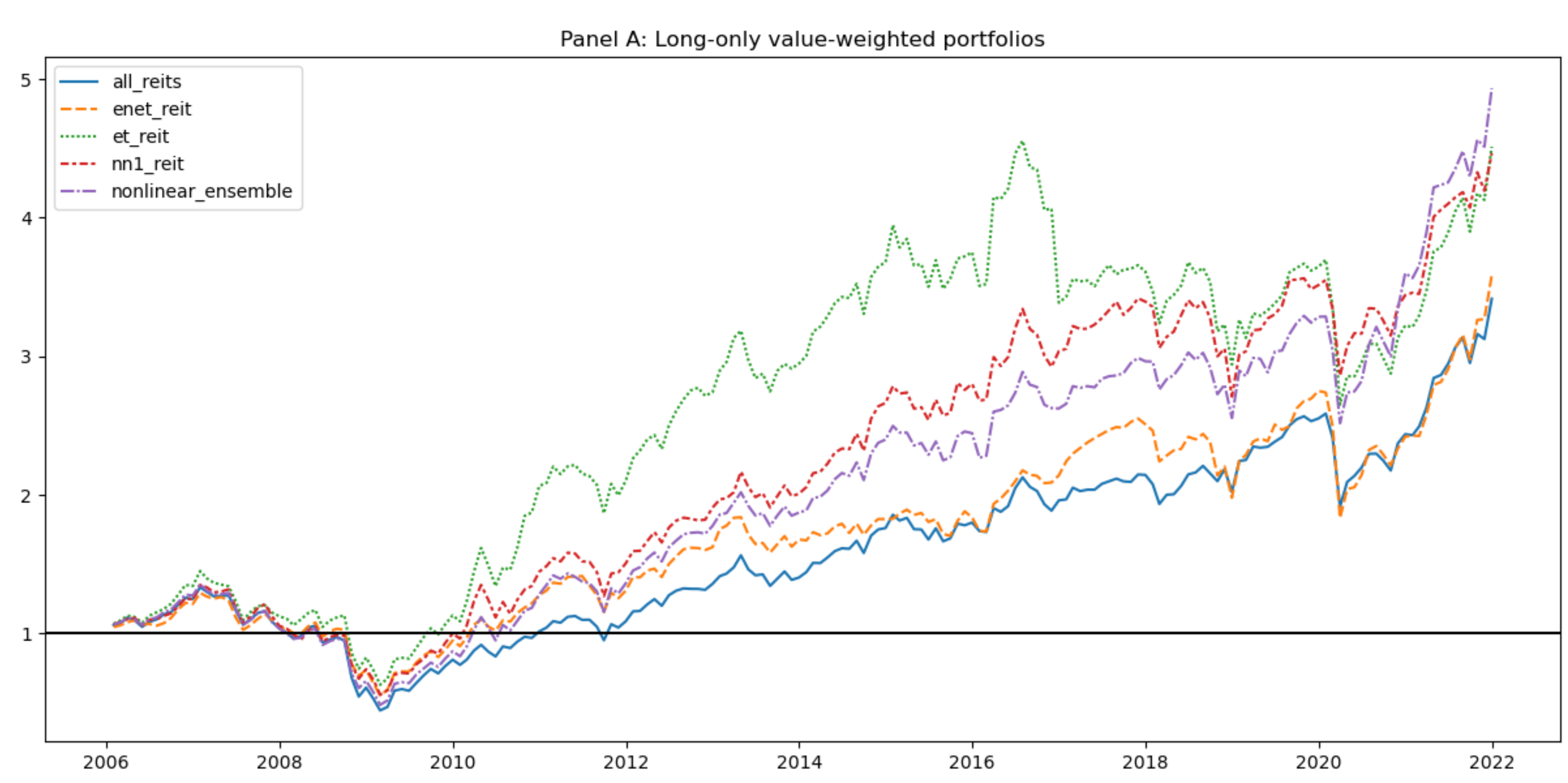

Missing data are pervasive in commercial real estate research, yet common practice remains to discard incomplete observations or fill gaps with crude imputat...

I have learnt a lot from David Geltner over the last 20 years.

This made me smile.

Piet Eichholtz and I wrote this short piece on the impact of changing demographics on house prices many years back. Some people still ask me for a copy, so I...

It happens so often, stings every time, and should not slow you down…

Maybe, someone has used this term before. If not, I would like to suggest “ultra-processed data.”

This year back in Gainesville, Florida, Oct 9-11. Apply before June 1st.

David Graeber’s ‘On the Phenomenon of Bullshit Jobs: A Work Rant’ made a compelling argument: many modern jobs exist for no real reason. Bureaucratic middlem...

Paper forthcoming in Real Estate Economics: We add to the emerging literature on machine learning empirical asset pricing by analyzing a comprehensive set of...

It’s easy to throw out bold ideas on how AI will change the real estate industry for good. But how can we prepare our students for an unknowable future? How ...

It was such a joy to welcome back our MPhil alumni and former colleagues for the 2024 MPhil reunion! I truly enjoyed the evening, hearing all about your impr...

As I sat in the dentist’s chair, waiting for the local anesthetic to kick in, I finally asked the dentist something I had wondered about a few times before: ...

The Cambridge Endowment for Research in Finance (CERF) has published a blog post on Kahshin Leow’s and my research on predictable REIT returns: https://www.c...

Spring has arrived both at home and at work.

This Wednesday (March 20) will be busy: First, I’ll head to the University of Reading for a research seminar (12–1 pm). My paper shows how REIT return predic...

Spring arrived early this year. The apricot is flowering, to the delight of big bumble bees. Let’s hope there will be no more frosty spells.

“In [Trump’s] world: rent regulated apartments are worth the same as unregulated apartments; restricted land is worth the same as unrestricted land; restrict...

Still looking for an easy new year’s resolution? Something that won’t be difficult to do but might make you feel better every time you navigate the Internet?

Want to run a large language model (LLM) on your computer? Llamafile makes hosting a LLM chatbot locally as simple as downloading a single file and starting ...

I spotted this exceptionally well-made gate not far from home. The oak wood has been hewn, not sawn, giving strength and elegant curves. Connections made in ...

Not ideal from a building maintenance point of view… but beautiful. A gutter has been leaking for years and created a truly ‘green’ building on Silver Street...

The Department of Land Economy is searching for one more Assistant Professor in Real Estate Finance. Here my thoughts on why this might be an attractive oppo...

New paper by Matthijs Korevaar explores the links between financial markets and real estate in 18th-century Amsterdam

An update from the garden: Tulips tulips tulips

Personal news: I have been elected Grosvenor Professor of Real Estate Finance at the University of Cambridge

Etchings by Franz Xaver Rektorzik, printed by August Potuczek

How do ML-models arrive at their predictions? Do they do what we hope they do—or are corners cut?. New paper out at Real Estate Economics

Staying in touch: A sporadic email with updates

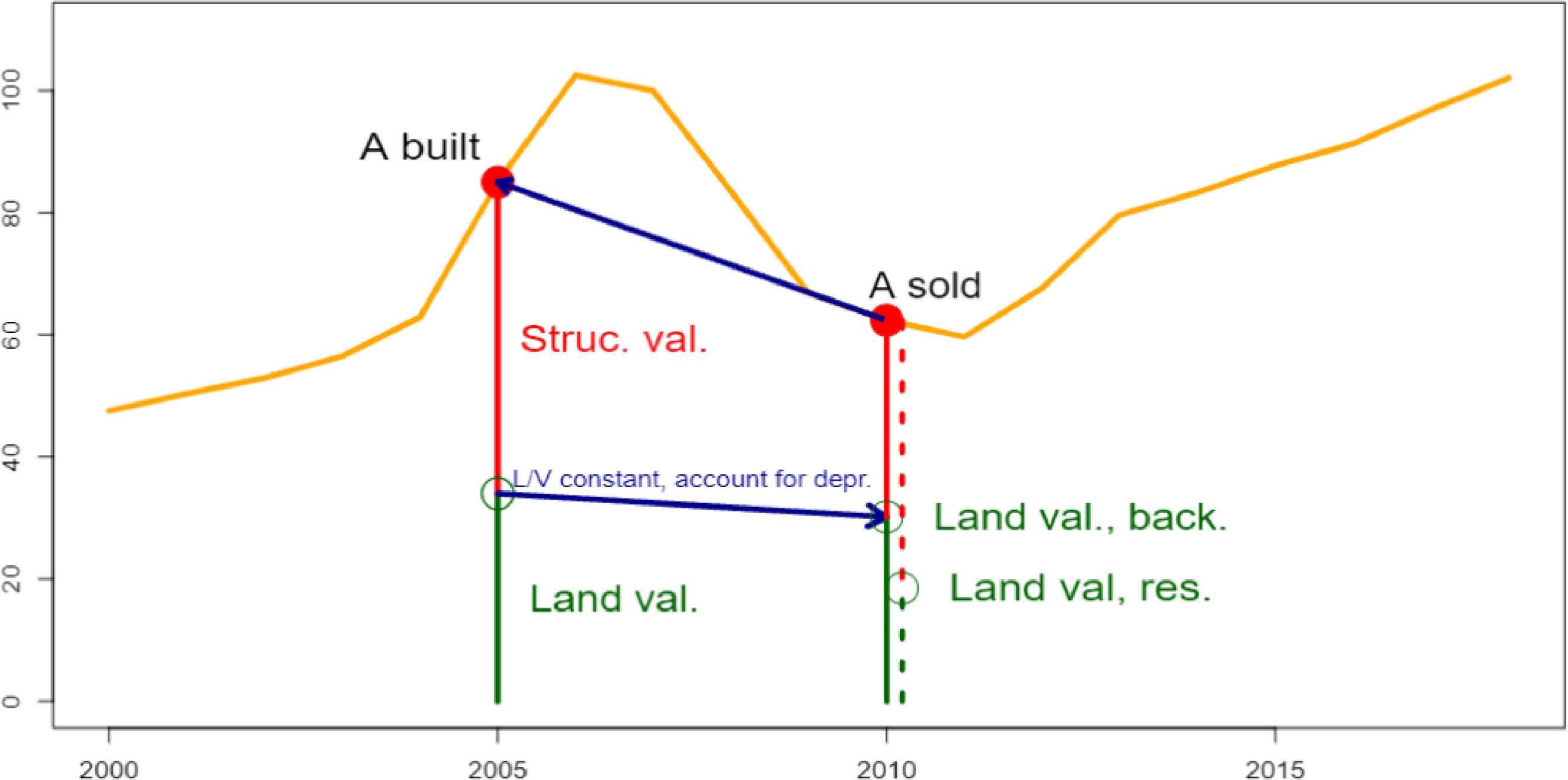

Paper out: This paper develops a new approach to estimate the value of urban land and indirectly tests land residual assumptions. Bonus: Value surfaces estim...

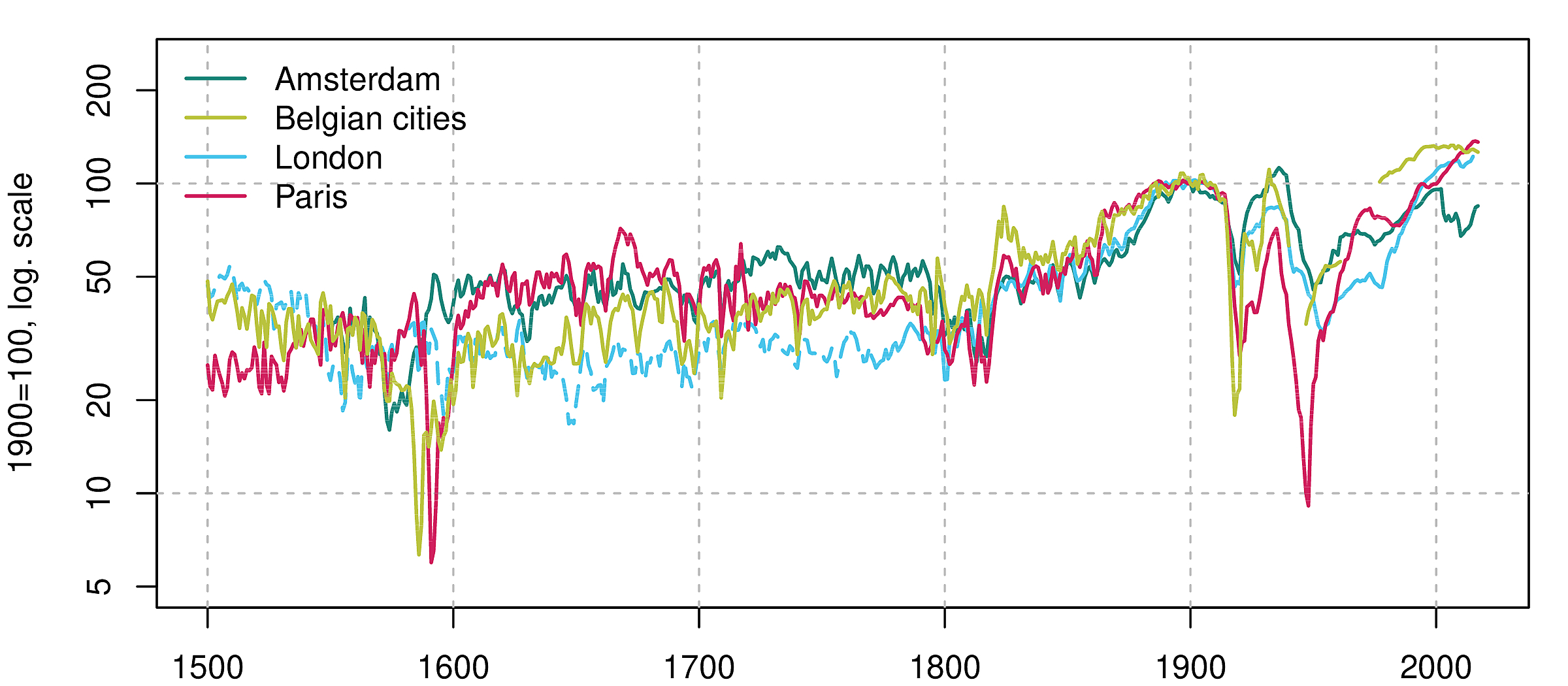

This paper studies urban rental prices for half a millennium (1500–2020) and seven cities: Amsterdam, Antwerp, Bruges, Brussels, Ghent, London, and Paris. Ba...

A neural networks that accounts for spatial correlation and time dynamics?

New paper out: A closer look at urban land and structure values – this is important for national accounts and for analysis of real estate risk over time. Wit...

Summary of our total return paper in German and French.

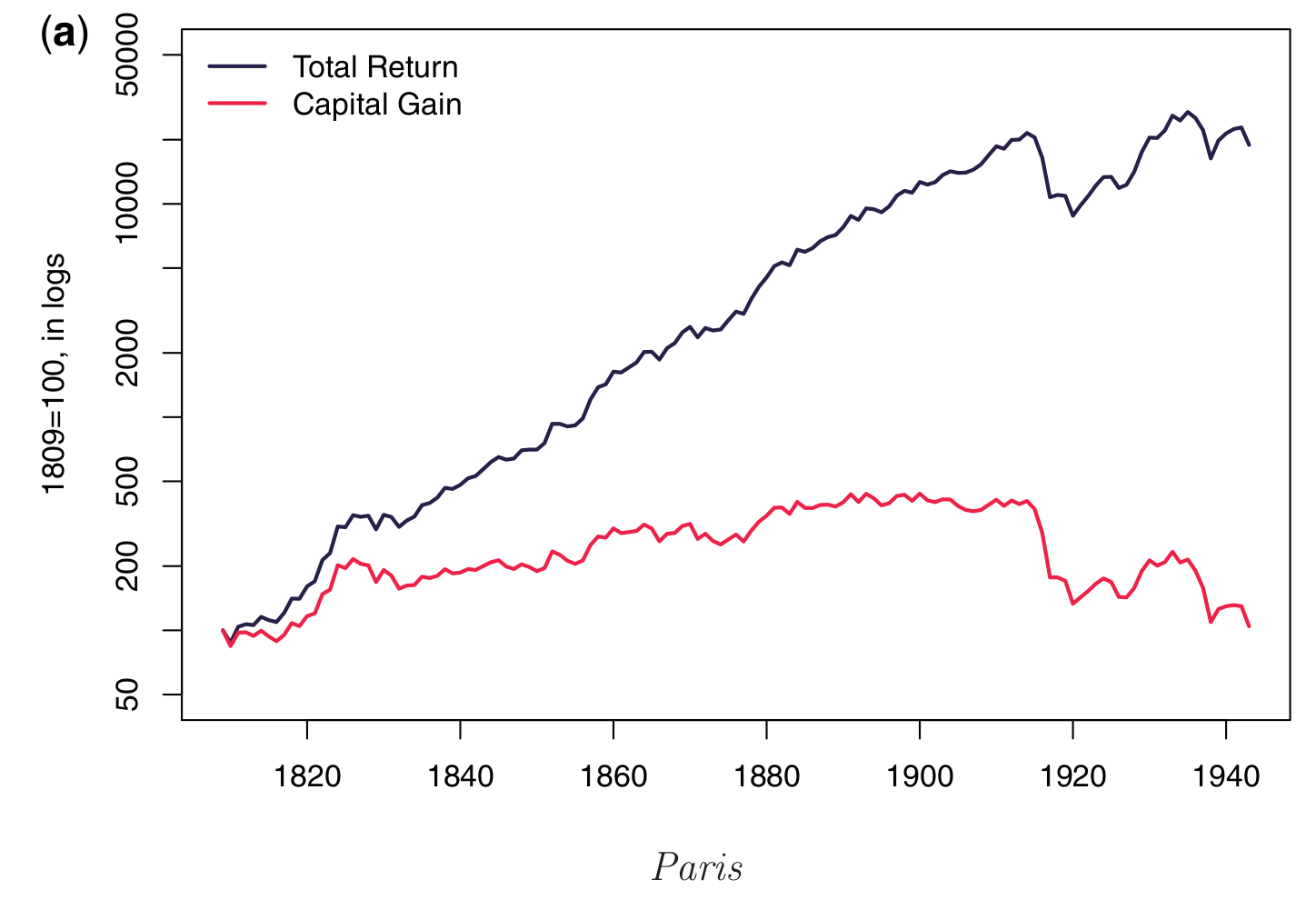

New research accepted for publication at the Review of Financial Studies (RFS) suggests that returns to real estate are solid but not exceptional: No sign of...

My previous website went down in flames (or rather: is now hosted in a black cloud).

New research accepted for publication at the Journal of Real Estate Finance and Economics: This paper couples a traditional hedonic model with architectural ...

This paper first collects binary classifications of house pictures from a large group of participants and then trains personalized ML classifiers for each pa...

This article estimates the first constant quality price index for Internet domain names. The suggested index provides a benchmark for domain name traders and...